Big Muni Spreads Don’t Mean Big Defaults

This article was originally published on eBooleant.com. Join readers who know that significant defaults are rare in the public sector.

Illinois Gov. J.B. Pritzker signed a $43 billion state budget with a huge hole from unfunded pensions and yet to be approved federal funding. Meanwhile the GOs of the state have yields hovering around the 4-5% range, far above the Treasury ten year rate. So the market is thinking default? Not so fast. We are learning to think of yield spreads as more than credit spreads in the COVID-19 era.

The Muni market response to the COVID-19 pandemic will be the subject to study for many years. Now, however, is not too soon to begin the analysis. It is particularly acute as we may be passing from the first to the second wave of the virus cycle.

An Efficient Muni Market?

The questions of first instance are often related to market returns and implicitly ask whether yield spreads accurately responded to an event. While this is of course important, it implicitly expects a version of informational market efficiency.

One difficulty is that market efficiency is at best asymptotically obtained. Markets are not informationally efficient in any classical sense as this period again shows. What prices signal when they become highly distorted is far from clear.

For municipals, traditional methods of relative value such as tax arbitrage are not at work here. One minus the marginal tax rate times the taxable rate is not a good guide to the yield on a tax-exempt bond. And pricing mechanisms are fundamentally altered by Federal Reserve Bank buying behavior.

Are Current Spreads Predictors of Default?

The aberrant behavior of credit spreads in the COVID age asks whether they reflect higher expectations of default, less liquidity, or issuer specific market segmentation effects. This is particularly important for Munis, a market with few significant defaults for their investor’s “safe money.”

For municipal bond investors, the question remains – do high municipal credit spreads imply higher expectations of default? We can get some guidance on this matter from a recent National Bureau of Economic Research study entitled When Selling Becomes Viral: Disruptions in Debt Markets in the COVID-19 Crisis and the Fed's Response. The authors found, in part, that:

“The safer end of the credit spectrum experienced significant losses that are hard to fully reconcile with standard default or risk premium channels. Corporate bonds traded at a large discount to their corresponding CDS, and this basis widened most for safer bonds. Liquid bond ETFs traded at a large discount to their NAV, more so for Treasuries, municipal bonds, and investment-grade corporate than high-yield corporate.”

The Past is the Future with the Fed

The role of liquidity and the Fed are emerging as significant factors in bond pricing performance. Liquidity or the lack of it replaced solvency as the primary determinant of spread behavior. Safe bonds, i.e. munis, suffered far greater credit spreads than can reasonably be justified by expected default behavior.

This was hardly the only novelty in bond pricing as the micro market features of the bond market dominated credit risk. One clear example was the cost of trading small lots versus blocks. The normative relationship was inverted as liquidity for larger blocks dried up and costs rose with block size. Nor should we expect a quick reversion to historical spreads. As the authors of the paper Anatomy of a Liquidity Crisis: Corporate Bonds in the COVID-19 Crisis say, “We argue that the Federal Reserve’s actions reflect a new role as market maker of last resort.” [1]

The interpretation of yields spreads is even more complex now with the Fed’s commitment to maintaining liquidity. The authors of another paper, The Corporate Bond Market Reaction to Quantitative Easing During the COVID-19 Pandemic, find that “bond illiquidity measures is consistent with the default risk channel of monetary policy in which the central bank’s commitment to support the credit market enhances overall economic prospect and thus reduces default risk of borrowers.”[2]

Thus, not surprisingly, the Fed lowers default generally. Muni bond market disruptions are not a good signal of future defaults. But this is only part of the COVID-19 problem. How did the muni market respond to the pandemic news? For this we suggest a different approach.

Look at the behavior of issuer risk aversion. Were issuers willing to accept the risk of higher leverage in the face of the pandemic? This is surely the result of many factors, including market acceptance for their bonds. Nevertheless, it introduces a different approach to the risk issue and allows us to ask if the reaction differed by the degree of infection across the states.

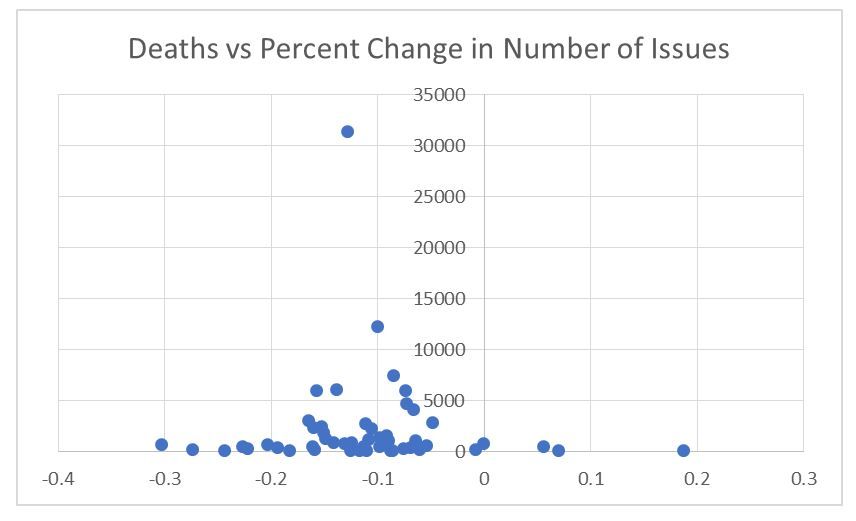

Because of the speed of events, my study here is preliminary in scope. If we look at the number of muni bond issues sold in May of 2020 versus May of 2019, we would expect fewer issues so the percent change is as expected negative. But the size of the reduction is not related to the number of COVID-19 deaths experienced in the state in 2020. See Chart 1.

Conclusion

The data so far is limited but consistent with the market responding to the general COVID-19 threat but not to state specific events. In this sense, munis spreads are not signaling new default concerns as much as generalized uncertainty.

[1] O'Hara, Maureen and Zhou, Xing (Alex), Anatomy of a Liquidity Crisis: Corporate Bonds in the COVID-19 Crisis (May 31, 2020). Available at SSRN: p. 17

[2] Nozawa, Yoshio and Qiu, Yancheng, The Corporate Bond Market Reaction to Quantitative Easing During the COVID-19 Pandemic (May 14, 2020). Available at SSRN

We hope you enjoyed this article. Please give us your feedback.